Interest Rate Update

Cash rate increases by 25 bps

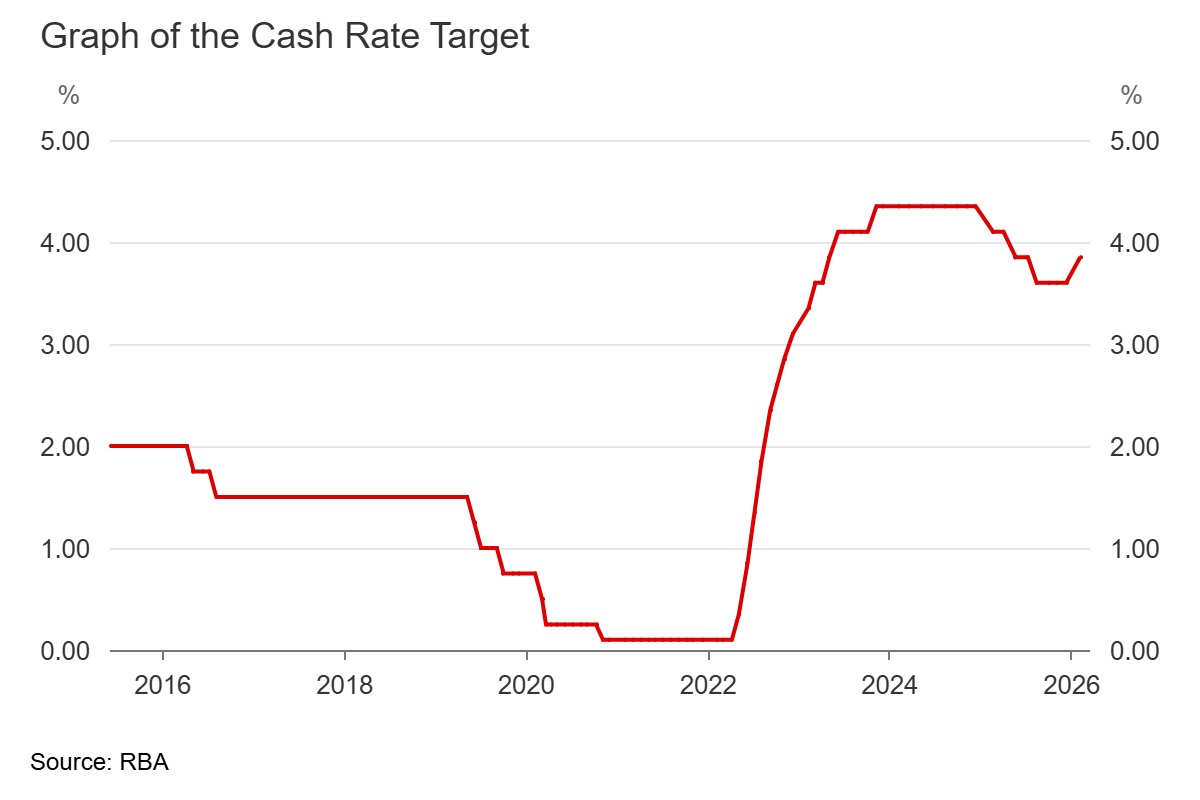

Australia continues to experience a period of persistently elevated underlying inflation, sustained wage growth, falling productivity growth and low levels of unemployment. These factors in combination with the outlook on global economic conditions prompted the interest rate setting board of the Reserve Bank of Australia (RBA) to raise the cash rate by 25 basis points to 3.85% at its February 2026 meeting.

Source: Reserve Bank of Australia, Cash Rate Target, https://www.rba.gov.au/statistics/cash-rate/, accessed 10/02/2026

The first rise in the cash rate since November 2023 followed a series of stronger than expected inflation readings across the second half of 2025, notably underlying inflation rose to 3.4% over the year to December (headline inflation was 3.6%), higher than predicted in prior quarterly forecasts and well above the 2% to 3% annualised target band. The RBA has been willing to look through temporary rises in volatile items such as fuel and food which is often impacted by commodity prices and fires, floods, and cyclones. However, sustained increases in services inflation are often stickier and a sign of a “hot” economy. The largest contributors to annual inflation over the past 12 months were Housing (+5.5%), Food and non-alcoholic beverages (+3.4%), and Recreation and culture (+4.4%). Within the housing group, Electricity (+21.5%), Rents (+3.9%) and new Dwellings (+3%) were the key drivers of inflation. Electricity was not unsurprising as the state and federal government household electricity subsidies from a year earlier ended. The increases in rental prices largely reflect a chronic undersupply and low vacancy rates in major cities, strong population growth from overseas migration and increases in landlord holding costs (i.e. strata levies, council rates, utilities etc..). Of Recreation and cultural, domestic holiday travel and accommodation rose 9.6% over the year as households travelled close to home[1].

In addition to inflation, the RBA is concerned about GDP growth in combination with growth in labour productivity. GDP growth was 2.1% over the year to the September quarter which was in line with expectations. Underlying data suggests private demand was especially strong in the second half of 2025 which will likely see the December quarter GDP number come in higher than 2.1% when the official figures are released on 4th March 2026. The RBA has been closely monitoring the growth in GDP in combination with the trend in falling labour productivity growth and increasing wages growth. Labour productivity growth has been on a declined since 2021 from 1.3% p.a. to 0.8% at the end of 2024. At the same time wage growth has increased from 1.3% at the start of 2021 to 3.4% at the end of September quarter. In simple terms, Australian wages are increasing at a faster rate per hour then their unit output per hour worked.

The unemployment rate was 4.1% in December, lower than the previous month’s 4.3% and market expectations, while the number of employed persons increased by 65,200 above the forecast of 30,000 and higher than the revised increase of 28,700 in the prior month. The tightness in the labor market provided more weight behind the need to raise interest rates.

The RBA emphasises the above economic indicators are a sign the recent pick‑up in inflation has been broadly based on the following factors:

- Strong private sector demand (households),

- Capacity constraints in supply,

- Activity in the housing sector.

Governor Michele Bullock, in her February press conference, stated that the RBA now believes it will take longer than previously expected for inflation to return to target. She described the persistence of inflation as “not an acceptable outcome,” reinforcing the Board’s willingness to act further if needed.

Current Interest Rate Path and Market Expectations

Financial markets and economists broadly anticipated the February increase, with consensus building around further tightening through 2026. The RBA’s February Statement of Monetary Policy notes that market implied expectations assume roughly 30 basis points of additional increases over the forecast period bringing the cash rate well above earlier projections of rate reductions. As of 9th February, the implied cash rate is expected to rise by 4.23% by September 2026.

[1] Consumer Price Index, Australia, https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation/consumer-price-index-australia/latest-release, accessed on 10/02/2026

Article by Emily Buckley

Associate Adviser

E: emily.buckley@qiwealth.com.au

P: (02) 8247 2700